AI CERTS

3 months ago

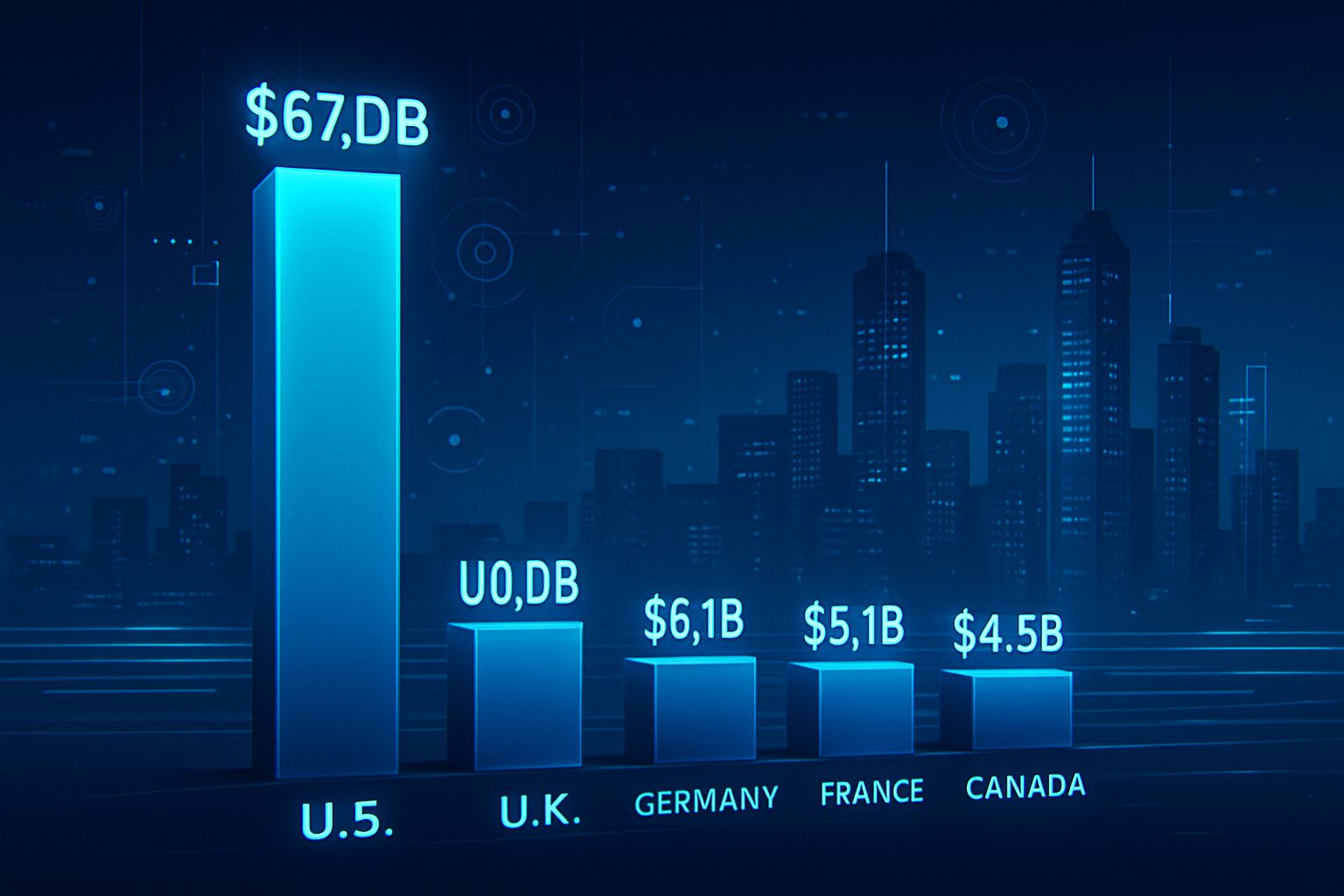

U.S. AI Drives Global Funding Dominance With $109.1B 2024 Surge

Consequently, understanding drivers, beneficiaries, and vulnerabilities behind the cash wave becomes essential for strategic planning. This article unpacks key actors, sectors, and policy levers underpinning the United States’ global funding dominance. Additionally, it evaluates venture capital concentration, hyperscaler spending trends, infrastructure buildout effects, and ecosystem maturity gaps. Each section concludes with concise insights and transitions, maintaining clear flow for busy professionals. Finally, actionable resources, including the Chief AI Officer certification, guide readers toward informed leadership.

Key Capital Surge Drivers

Stanford’s 2025 AI Index attributes 71 percent of 2024 private funding to late-stage U.S. rounds. Furthermore, mega-deals for foundation model developers such as OpenAI and Anthropic captured media attention alongside institutional allocations. Consequently, market narratives around global funding dominance intensified as deal sizes dwarfed European and Asian counterparts. Meanwhile, Microsoft’s planned $80 billion data-center spend illustrates how corporate capex rivals traditional venture flows. Jensen Huang emphasized demand, stating, “The age of AI is in full steam,” after Nvidia posted record revenue. However, Sam Altman warned investors about possible bubble conditions, reminding stakeholders of cyclical capital cycles. These signals reveal demand pull from both clients and suppliers. Therefore, the next section dissects hyperscaler spending patterns fueling compute capacity.

Current Hyperscaler Spending Trends

Hyperscaler spending crossed historic levels as Microsoft, Amazon, Google, and Meta raced to deploy advanced clusters. Additionally, more than half of Microsoft’s announced budget will remain on U.S. soil, reinforcing geographic clustering. In contrast, Chinese cloud providers face export-control constraints, widening the domestic capacity gap. Consequently, global funding dominance is reinforced through exclusive access to cutting-edge GPUs and electricity contracts. Nvidia’s Blackwell launch signaled continued hardware innovation, yet supply remains scarce, amplifying price premiums.

- Microsoft: $80 billion fiscal 2025 AI data-center commitment

- Nvidia: $30.8 billion quarterly data-center revenue

- Generative AI private funding worldwide: $33.9 billion

- U.S. share of private AI deal value: 71 percent

Moreover, these figures highlight venture capital concentration around compute infrastructure rather than consumer applications. Hyperscaler allocations represent long-term fixed commitments that stabilize supplier roadmaps. Next, we examine economic ripples from the infrastructure buildout.

Infrastructure Buildout Economic Impacts

Infrastructure buildout drives demand for land, power, fiber, and skilled labor across multiple U.S. regions. Consequently, states like Iowa, Virginia, and Texas court data-center incentives to capture taxable assets. Moreover, utilities negotiate multiyear contracts, ensuring predictable cash flows yet stressing local grids. Stand-alone startups also benefit; cloud-GPU providers lease capacity to smaller labs lacking capital intensity. Nevertheless, critics argue concentration worsens environmental footprints and increases single-point failure risk. Therefore, global funding dominance may falter if community pushback slows permitting for new megawatt campuses. Economic multipliers appear significant, yet externalities persist. The funding structure itself deserves inspection, starting with venture capital concentration.

Rising Venture Capital Concentration

Venture capital concentration intensified as top ten funds supplied over 60 percent of 2024 deal value. Furthermore, crossover hedge funds reentered growth rounds, chasing perceived asymmetric upside on generative AI. In contrast, seed-stage activity flattened, suggesting capital bypasses earliest experiments in favor of scale economies. Consequently, startups outside elite networks struggle to access compute credits and mentoring. Sam Altman’s bubble warning underscores how such skewed flows could trigger painful repricing. Nevertheless, investors anticipate outsized exits as cloud giants acquire specialized tooling and safety platforms. Capital clustering magnifies both risk and reward. Attention now shifts toward ecosystem maturity as deployment accelerates.

Assessing Ecosystem Maturity Challenges

Ecosystem maturity involves governance, talent pipelines, security baselines, and responsible-AI adherence. Moreover, 78 percent of surveyed enterprises reported AI use in 2024, yet standardized safety audits lag. Consequently, regulatory agencies propose voluntary watermarks and incident-response reporting. Meanwhile, the White House memorandum outlines procurement preferences for evaluated models, nudging suppliers to mature quickly. However, Stanford researchers note responsible deployment remains uneven even amid global funding dominance.

- Share of firms with ethics review boards: 34 percent

- Percentage of models releasing system cards: 27 percent

- Organizations offering AI literacy training: 49 percent

Additionally, professionals can enhance oversight skills with the Chief AI Officer™ certification. Maturity gaps threaten trust and adoption. Finally, policy direction and risk considerations frame possible futures.

Policy And Risk Outlook

Federal initiatives like NAIRR and CHIPS funding aim to democratize access and shore security. Additionally, export controls restrict advanced GPU shipments to adversarial jurisdictions, preserving domestic advantages. Nevertheless, geopolitical retaliation could disrupt supply chains, challenging infrastructure buildout timelines. Consequently, investors monitor legislative calendars alongside market indicators to gauge sustainability of global funding dominance. In contrast, bold domestic spending may crowd out private R&D if regulatory burdens mount. Therefore, balanced public-private collaboration remains essential to maintain innovation velocity. Policy moves will shape capital allocation and risk distribution. Forward-looking leaders must prepare adaptable strategies.

In summary, U.S. investors, hyperscalers, and policymakers collectively forged global funding dominance through unprecedented capital flows, ambitious infrastructure buildout, and concentrated venture strategies. Moreover, hyperscaler spending and venture capital concentration continue reinforcing the lead while creating systemic exposures. Nevertheless, advancing ecosystem maturity and prudent policy can sustain global funding dominance for another innovation cycle. Therefore, executives should monitor capex signals, regulatory developments, and responsible-AI benchmarks. Act today by exploring certifications and strategic partnerships that position your organization at the frontier of AI value creation.