AI CERTS

5 months ago

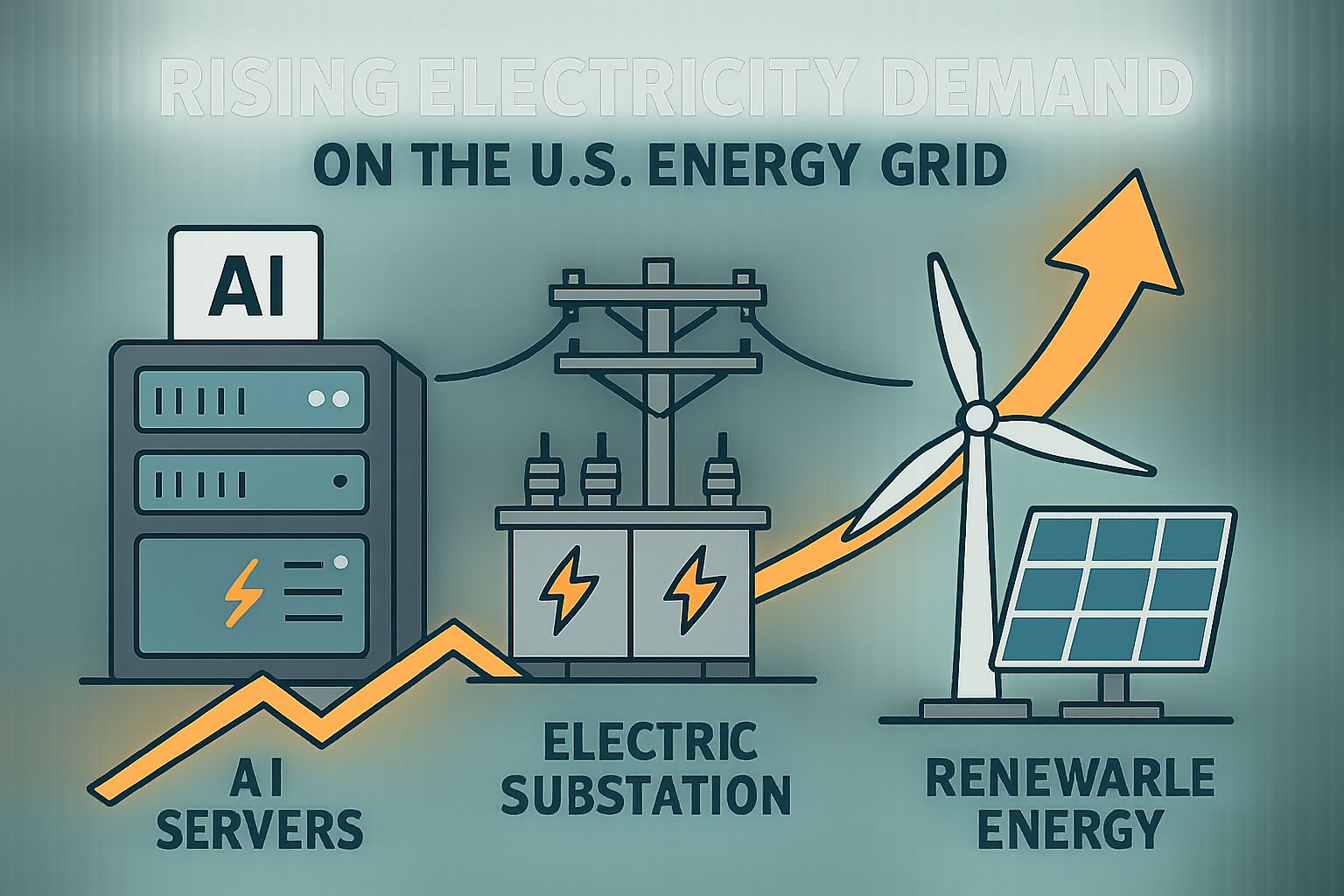

AI Workloads Push US Grid Demand To New Heights

Meanwhile, North American pipelines for new capacity have exploded. Regional planners now treat AI facilities as the largest incremental load in decades. This article unpacks numbers, debates, and emerging solutions guiding industry strategy. Professionals will gain data, context, and policy signals amid rapid Electrification. Stronger insights begin below.

AI Load Reshapes Planning

IEA’s 2025 'Energy and AI' study projects 945 TWh for global computing sites by 2030. Accelerated servers are growing roughly 30% annually, dwarfing historic averages. Therefore, planners must revisit load models for US Grid Demand immediately.

EIA data, reported by Reuters, shows national consumption records arriving in 2025 and 2026. Meanwhile, PJM forecasts a 32 GW peak jump, with 30 GW tied to Data Centers. ERCOT lists 205 GW of large-load requests, over 70% from AI facilities. Consequently, transmission studies are overwhelmed.

Demand curves now bend upward faster than generation schedules. However, regional patterns differ sharply, leading to our next focus.

Regional Impacts Intensify Fast

Northern Virginia hosts the world’s densest concentration of Data Centers today. PJM warns capacity auctions may spike unless flexible resources appear. Resulting US Grid Demand concentrations outpace available transmission. Additionally, lawmakers urged stricter backstop rules to protect ratepayers.

Texas tells a parallel story. ERCOT’s interconnection queue ballooned after AI developers filed speculative requests. In contrast, state legislation now demands disclosure and potential curtailment rights.

Midwestern utilities negotiate unique contracts, offering priority hookups for voluntary curtailment. Google’s Indiana Michigan agreement showcases that model.

Region-specific politics shape every tariff and timeline. Consequently, financial stakes escalate, which we examine next.

Economic Stakes Mount Rapidly

Goldman Sachs pegs required grid investment at $720 billion through 2030. Deloitte forecasts AI power needs climbing from 4 GW to 123 GW domestically. Such projections assume continued 26% Growth in compute intensity and facility count.

- Goldman: 165% rise in US Grid Demand scenarios

- IEA: 130% data-center power increase between 2024 and 2030

- PJM: 32 GW peak load gain; 94% from Data Centers

- ERCOT: 205 GW of pending large-load requests

- CBRE: 34% market supply expansion, vacancy 1.9%

Capacity prices already reflect tightening reserves in PJM auctions. Therefore, corporate buyers sign longer contracts to hedge volatility.

Capital markets now treat reliable energy as a gating factor for AI scale. Nevertheless, reliability concerns run deeper, discussed in the following section.

Grid Reliability Risks Surface

Large contiguous loads shorten reserve margins during summer peaks. PJM’s board launched a Critical Issue Fast Path to develop new rules. Meanwhile, consumer advocates worry about cost socialization. Forecast models show US Grid Demand spikes coincide with summer peaks.

Reliability planners fear simultaneous AI training cycles across multiple regions. However, flexible scheduling of non-urgent workloads offers hope.

Google claims demand response can shift megawatts within minutes when frequency drops. Such agility supports Electrification without compromising service levels.

Reliability hinges on contracts, technology, and policy alignment. Therefore, mitigation tactics warrant closer inspection next.

Strategic Mitigation Tactics Emerge

Developers pursue three complementary strategies. Firstly, they design liquid cooling to improve efficiency and lower site power usage. Secondly, renewables plus storage help counterbalance training cycles. Thirdly, dynamic workload shifting creates virtual elasticity across campuses.

Demand response contracts illustrate practical cooperation between utilities and hyperscalers. Consequently, Google paused machine learning jobs during recent Midwestern heat waves. Flexible contracts directly target US Grid Demand volatility. Professionals may deepen skills through the AI Foundation™ certification.

Electrification strategies also include on-site microgrids and fuel-flexible turbines. Nevertheless, advocates warn about carbon lock-in if gas dominates.

Flexible design lowers costs and emissions simultaneously. Moreover, policy triggers will influence adoption, described next.

Policy Watchlist Items Expanding

Federal regulators may receive filings from PJM detailing mandatory capacity backing rules. ERCOT continues revising interconnection study processes amid stakeholder pressure. Subsequently, several states debate cost allocation for transmission upgrades.

Congressional letters already criticize rapid cost pass-through to households. In contrast, industry groups advocate streamlined permitting and tax credits.

International observers track these debates because U.S. precedents often set global norms. Therefore, forecasting US Grid Demand requires parallel policy analysis.

Policy momentum will shape investment decisions within months. Consequently, stakeholders must understand possible scenarios, explored in the final section.

Future Outlook Pathways Ahead

Scenario modeling suggests divergent futures based on technology adoption speed and regulatory support. One baseline expects sustained 26% Growth in AI server shipments through 2030. Under that path, US Grid Demand might rise another 30 GW inside PJM alone.

A moderated case uses efficiency gains to flatten curves despite continued Electrification. Nevertheless, even that variant still pushes many utilities into accelerated resource planning.

Google and peers signal willingness to align workloads with renewable peaks. Moreover, advanced forecasting software can route tasks to regions with spare capacity. Data Centers increasingly operate like mobile power consumers, following cheap electrons.

The chosen pathway will decide capital flows, emissions trajectories, and competitive advantage. Therefore, precise monitoring of leading indicators remains essential.

Key Takeaways And Actions

AI acceleration is rewriting energy forecasts. Record interconnection queues, volatile capacity prices, and urgent policymaking underscore the pivot. Consequently, US Grid Demand sits at the center of boardroom discussions. Stakeholders must gauge 26% Growth assumptions, Data Centers siting patterns, and Electrification policies carefully.

Practical solutions already exist. Demand response, flexible cooling, and on-site renewables can mitigate reliability concerns. Furthermore, educated professionals drive adoption faster. Consider the AI Foundation™ certification to strengthen cross-disciplinary understanding.

Monitor PJM filings, ERCOT reforms, and federal incentives over the coming quarters. Ultimately, proactive engagement will convert surging US Grid Demand into sustainable opportunity.

Disclaimer: Some content may be AI-generated or assisted and is provided ‘as is’ for informational purposes only, without warranties of accuracy or completeness, and does not imply endorsement or affiliation.